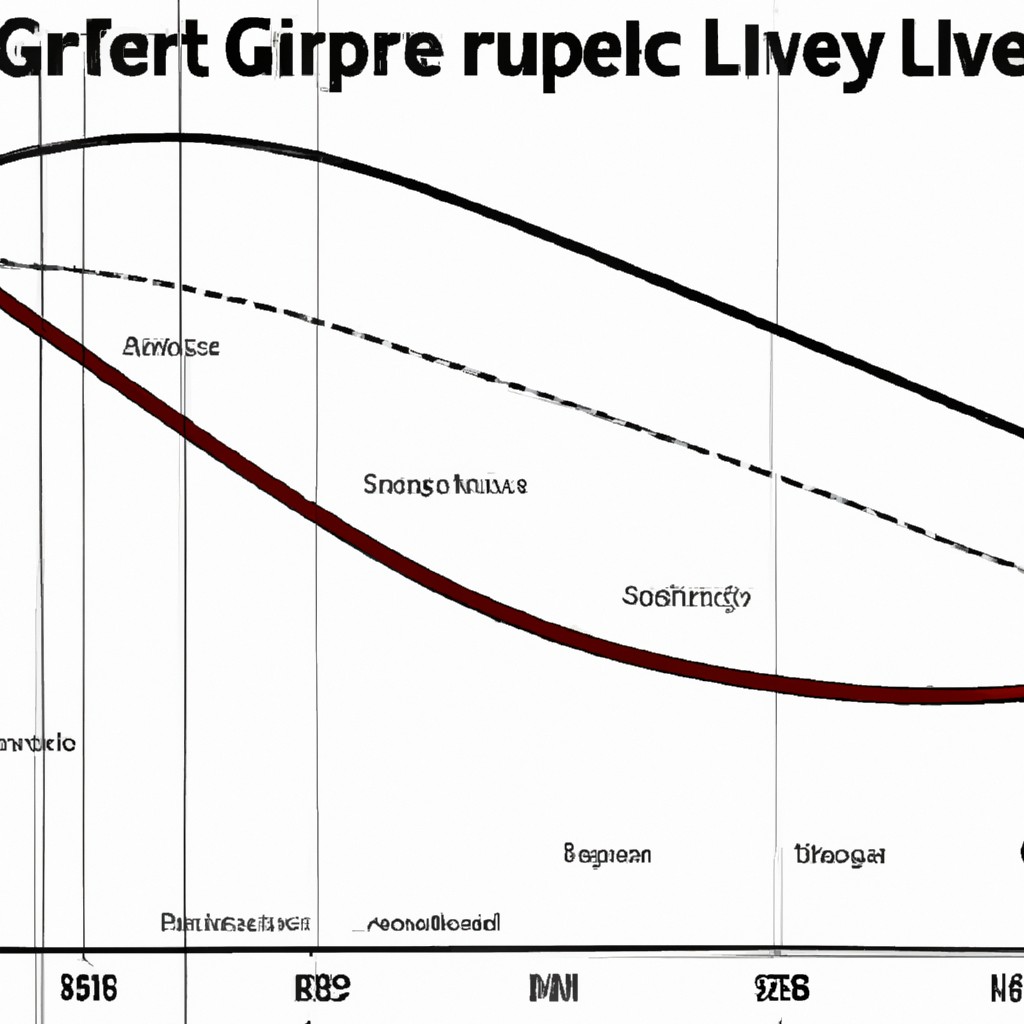

Steps to construct a Lorenz curve

To construct a Lorenz curve, plot cumulative percentage of total income against cumulative percentage of population. Represent perfect equality as a straight 45-degree line. Calculate the Gini coefficient from the Lorenz curve. Use the formula of Gini coefficient, a quotient of the area between the Lorenz curve and the line of perfect equality divided by the total area under the line of perfect equality. Interpret the Gini coefficient as a measure of income inequality. A higher Gini coefficient indicates greater inequality, while a lower coefficient represents more equality. Illustrate income distribution patterns through the Lorenz curve and Gini coefficient analysis.

Read more

Calculation steps for Theil index

The Theil index is a way to measure inequality. First, calculate base values for each group. Then, compute the natural logarithm of the ratio between group values. Next, sum the products of ratios and log values. Finally, divide by the total population to obtain the Theil index.

Read more

Calculation steps and methodology

When starting a calculation, first gather all necessary information. Next, identify the required steps. Then proceed to perform the calculations accurately. Verify the results for correctness. If needed, double-check calculations. Ensure to use a reliable method. Regular practice improves calculation accuracy. Remember to stay focused and avoid distractions. Following these steps will lead to effective and precise calculations.

Read more

Steps to take when filing an Insurance claim.

When filing an insurance claim, there are several important steps to take. First, gather all necessary documentation, such as policy information, incident reports, and photos of any damage. Next, notify your insurance company promptly and provide all details of the incident. Be prepared to answer any questions they may have. It is crucial to follow any instructions provided by your insurance company, such as obtaining repair estimates or submitting additional documentation. Keep a record of all communication and correspondence with your insurance company. Finally, be patient throughout the process, as it may take time for your claim to be processed and resolved to your satisfaction.

Read more

Steps for conducting case studies

Case studies are a valuable research method used to analyze real-life situations and gather in-depth information. Here are the steps for conducting effective case studies. Firstly, define the research question or objective to focus the study. Next, select the appropriate case or cases that align with the research topic. Then, collect data using various methods such as interviews, observations, and document analysis. After gathering data, analyze it thoroughly to identify patterns, themes, and key findings. Present the findings in a clear and concise manner, using visuals if necessary. Lastly, draw conclusions and discuss the implications of the study in relation to existing literature. By following these steps, case studies can provide valuable insights and contribute to knowledge in various fields.

Read more

Steps in the cost-benefit analysis process

When conducting a cost-benefit analysis, several steps should be followed to ensure accurate results. Firstly, clearly define the problem or decision needing evaluation. Next, identify and develop a list of all costs and benefits associated with the decision. It's important to include both tangible and intangible factors. Then, assign a monetary value to each cost and benefit item, taking into account any uncertainties or risks. Afterwards, calculate the net present value, which compares the total present value of benefits to the total present value of costs. Lastly, interpret the results, considering the overall feasibility and desirability of the decision. This systematic approach helps decision-makers make informed choices while considering the financial implications.

Read more